Mortgage Forbearance in Northern Ireland: Lender vs. Borrower Perspectives

When an interest-only mortgage term ends with a shortfall, both borrowers and lenders are placed in a very difficult position.

Here's a contrasting summary of how current mortgage forbearance legislation and processes in Northern Ireland impact each party.

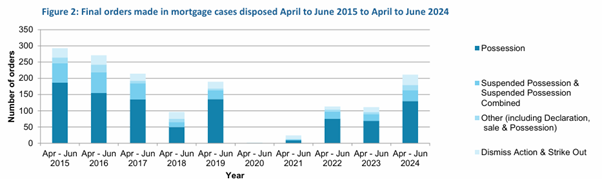

There is currently a huge increase in mortgage debt in NI. During the quarter April to June 2024, there were 211 final orders made in mortgage cases disposed, which is a 90% increase on the number disposed of in the Chancery in 2023 (111) and a 38% decrease compared to the same period in 2007 (340).

Lender Perspective

Forbearance legislation generally favours lenders, as they are legally entitled to recover the outstanding mortgage debt. While forbearance measures may delay enforcement, they ensure that lenders can eventually reclaim what is owed.

Key advantages include:

- Protection of Financial Interests: Lenders can pursue full repayment through extended negotiations, securing the mortgage shortfall or repossessing the property if needed.

- Flexible Repossession Options: While forced to consider forbearance first, lenders can still seek repossession if no satisfactory repayment plan is reached.

- However, forbearance may delay recovery: Lenders face delays in recovering the debt due to mandatory forbearance options like payment holidays or restructuring.

Borrower Perspective

For borrowers, the forbearance process provides temporary relief but often fails to fully resolve the underlying issue of the shortfall.

Key benefits include:

- Borrowers get time to explore options such as extending the loan term, switching to a repayment mortgage, or arranging a settlement.

- Legislation ensures that lenders must offer forbearance options like restructuring or repayment holidays before initiating repossession.

However, borrowers face challenges:

- Lack of Permanent Solutions: Forbearance often delays the inevitable rather than eliminating the debt, especially if the borrower has limited ability to repay the shortfall.

- Additional Costs: Extending the mortgage term or switching to a repayment plan may increase the borrower’s overall financial burden.

https://www.nidirect.gov.uk/articles/mortgage-arrears-or-payment-difficulties

Borrower’s Potential Options When a mortgage shortfall occurs

Borrowers have several options:

- Restructuring the Mortgage: Extending the term or switching to a repayment mortgage can ease immediate pressure but requires stable future income.

- Negotiating a Settlement: Borrowers can negotiate a reduced lump-sum settlement with the lender if they can gather some funds.

- Sale of Assets: In cases of significant shortfall, borrowers may need to sell other assets or consider downsizing their home to cover the debt.

- Voluntary Repossession: Borrowers unable to repay may opt for voluntary repossession, where the lender sells the property, but this may still leave a shortfall to pay.

Sell and rent back possesses additional challenges.

Conclusion: Lender or Borrower?

Forbearance processes in Northern Ireland provide temporary relief for borrowers but ultimately benefit lenders by ensuring eventual recovery of the debt. Borrowers gain short-term breathing space but often face long-term challenges in resolving the shortfall. The key for borrowers is to act early, exploring all available options to avoid repossession or prolonged financial hardship.

For more information on mortgage forbearance, you can refer to the FCA link on mortgage shortfalls.

Advice NI has a referral partnership with Housing Rights. By completing the correct referral form and emailing direct to referrals@housingrights.org.uk whereby Housing Rights contact your referred client within three working days – please note Housing rights cannot assist with buy to let properties.